Many startup ventures need to raise seed funding from investors in order to achieve growth. This is definitely a challenging — often time-consuming — process. Here we try to demystify it and offer some guidance.

The exact definition of seed funding can vary by region and change depending on who you ask, and sometimes it is used generally to mean early-stage financing. Here, we’re going to talk about seed funding in terms of the “seed stage” and “seed round” as many investors refer to it.

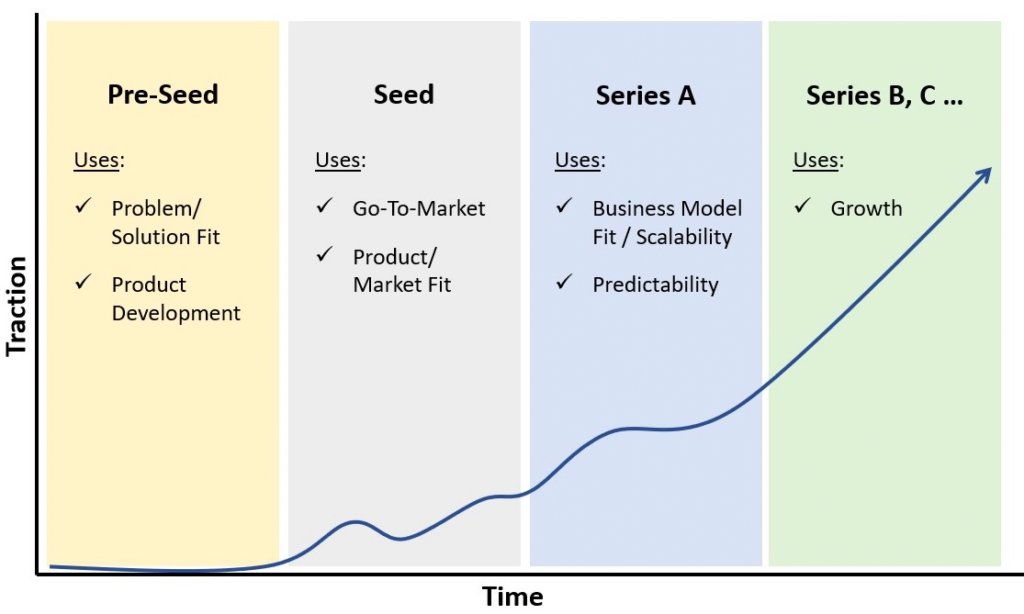

In this regard, seed funding, or a Series Seed Round, typically comes after a pre-seed funding round (typically comprised of friends, family, founders, and early angels) and before a Series A round. The seed round is sometimes thought of as the first institutional round of capital, during which established angel investor groups and early-stage venture capital (VC) firms invest. It’s also the go-to-market stage of the company which initializes the search for product-market fit.

Seed Round Characteristics

The average seed round size is usually in the $1 – 2 million range. The funding typically comes from multiple parties, which can include individual angel investors, angel groups, micro-VCs, accelerators, and perhaps some non-dilutive grant funding.

Most seed stage investors are interested in ventures that have a commercial-ready product and some early traction with customers. Many will want to see initial revenue, and recurring revenue with software-as-a-service (SaaS) companies.

Seed funding is used primarily to support sales, marketing, product support, and continue product development, as the company goes to market. Companies will add headcount and attempt to grow and retain their customer base.

The primary goal (a.k.a. milestone) of the seed stage is to reach product-market fit (PMF). Entrepreneurs need to develop, execute, and iterate on their product, market, and sales process until they get to PMF and position the company for a Series A funding, within the timeframe (a.k.a. runway) enabled by the funding. (Read more about Product-Market Fit).

As part of the round, the company will sometimes form a three- or five-person board of directors. The board will include at least one member of the funding group, which will have a say in the governance of the company going forward.

Investment Types

Seed investors commit capital primarily through either convertible debt or preferred equity. SAFE notes (simple agreement for future equity) are also an option, although are more popular on the coasts. Some investors will have a strong preference for a specific type, while others are more open.

Sometimes the choice of investment vehicle is straightforward. Pre-revenue startups usually opt for a note structure to defer the valuation until there’s something more to value. For post-revenue startups though, preferred stock is often the way to go, as it can put the company on firmer ground going into Series A. It’s also okay to discuss the choice with potential investors before making a decision.

Here are some pros and cons to each type:

Convertible Debt

Pros

Fast, easy, and low-cost to execute. Convertible note agreements are short and fairly standard. They don’t lock in a valuation of the company, which allows entrepreneurs time to grow the pie before diluting their ownership interest. Convertible notes also save time by pushing the valuation question down the road.

Cons

Notes accrue interest like any debt, which can quickly add up. Most also have a conversion discount of 10 – 25 percent, allowing investors to convert to equity at a lower share price. They also have a maturity date by which they’re supposed to be paid back or converted to equity. This can create challenges if the notes haven’t converted by maturity and if the startup lacks the cash to pay them off. Finally, some investors don’t like notes because they lack voting rights and leave their value undetermined. However, many notes offer a valuation cap that puts a ceiling on the pre-money value at which they will convert, which can alleviate investor concerns.

Preferred Equity

Pros

Preferred equity sets a valuation on the company which provides certainty for both investors and founders. Everyone knows where they stand in their ownership of the company. This also simplifies things going into a Series A round by avoiding potential complications with note conversions.

Cons

Negotiating a pre-money value can sometimes be a sticking point in a preferred equity financing (for more on valuation, see Primer on Tech Startup Valuation). Many other deal terms need to be worked out as well, including board composition, anti-dilution, etc., in the term sheet. In general, equity financing is more complex, with multiple agreements, which also increases legal costs.

SAFE Note

Pros

Like convertible debt, SAFE notes are fast, easy, and low-cost to execute. SAFE agreements are standard and even shorter than convertible notes. They also allow founders and investors to punt on valuation until the next round. However, SAFEs do not accrue interest and do not have a maturity date.

Cons

SAFE notes are still relatively new and unfamiliar to many investors, particularly in the Midwest, which can make fundraising more challenging. Also, many investors do not appreciate the lack of interest and maturity date. In addition, this complicates how they’re viewed by accountants, which have not yet standardized how to treat SAFEs on the balance sheet because they’re neither debt nor equity. They do typically offer a conversion discount into the equity round and have a valuation cap.

Investment Sources

As mentioned, there are multiple potential sources of investment for the seed funding round, including angels, angel groups, micro-VCs, accelerators, and grants.

Angel investors are high-net-worth individuals who invest in startups. Many also enjoy working with startups as mentors, advisers, and potential board members. In addition to funding, angels often provide a wealth of insight and experience, as well as access to their networks. Some work individually, while many benefit from participating in groups that provide access to deal-flow, shared knowledge, teamwork on due diligence, and additional capital which helps de-risk investments. Michigan has many established angel groups throughout the state. You can visit the Michigan Angel Community for more information.

Venture capital firms manage money on behalf of larger institutional investors like pension funds and endowments. Most large VC firms don’t come in until Series A, Series B, Series C, or later. But smaller funds managing under $50 million in capital — sometimes called micro-VCs — will invest in the seed round. There are many of this type of venture capital firm in Michigan, the Midwest, and nationally. For more information on venture capital in Michigan, check out the Michigan Venture Capital Association’s Michigan Entrepreneurial & Investment Landscape Guide.

In Michigan, there are also two state-backed groups that do pre-seed and seed financing — the First Capital Fund managed by ID Ventures and the Michigan Rise Pre-Seed Capital Fund III.

Accelerators may be another source of funding. There are many reputable accelerators (Y-Combinator, TechStars, 500 Startups, etc.) that are known nationally, including industry-specific programs, and local programs like the Desai Accelerator and Ann Arbor SPARK Entrepreneur Boot Camp. Most of these offer intensive short-term training for startups, and many offer seed funding as part of the package. Some accelerators also provide access to great networks that help set you up for future Series A and Series B funding.

Grant programs like the SBIR / STTR program, as well as Michigan’s Business Accelerator Fund and Emerging Technologies Fund programs, offer non-dilutive funding opportunities that can help you fill out your seed round without giving away ownership in the company.

For more on capital sources, check out A Few Fundraising Basics for New Startups.

Tips on Raising Seed Funding

Now that you know the basics of seed funding, here are some tips on raising the round:

- Understand the business opportunity in front of you and decide if you’re willing to commit potentially years of your life to it. If you bring on outside investors, they will expect your commitment to them and to a profitable return.

- Develop great fundraising materials including a pitch deck, executive summary, and a five-year proforma. (See Tips on How to Improve Your Pitch Deck).

- Practice your pitch with friends, family, and colleagues. Maybe you’ve already done that by successfully raising pre-seed money. Either way, know your business inside-and-out and be prepared for tough questions (hopefully ones you’ve already answered satisfactorily for yourself).

- Do some research on which groups to approach. Generate a list of investors that invest at your stage and in your industry by talking to people in your entrepreneurial ecosystem and with online resources (AngelList, Crunchbase, etc.). VCs have specific stage and industry criteria.

- Leverage your network to get warm introductions to these investment groups as best as you can. Seed investors may see hundreds of startups in a year — a warm lead helps break through the noise.

- Be persistent, patient, and passionate. Fundraising can be a time-consuming process and not every pitch will turn into an investment. Sometimes your company just won’t be a fit for that group’s model. If you’re persistent and show your passion and commitment for the opportunity, you’ve got a good shot.

- Be coachable and willing to take feedback during the fundraising process, which can go a long way.

Best of luck to you and we look forward to hearing about your $50 million Series C funding in a few years!